Dutch Tulip Mania and Bitcoin: Crystallizing Revolutions

A Bitcoin Lens on Peter M. Graber’s, Famous First Bubbles

It is “a certain propensity in human nature... the propensity to truck, barter, and exchange one thing for another... Humans, left to their own devices, will inevitably begin swapping and comparing things.” — Adam SmithBefore we can speak of bubbles, we need to clarify what an investment is. It is a calculated risk for a calculated potential gain.

A bubble is when that risk is “irrationally exuberant,” as Alan Greenspan, former Chairman of the Board of Governors of the Federal Reserve, calls it. Mr. Greenspan called the Dow at 6500 points in 1996 “irrationally exuberant.” When the Dow was up 50% three years later in 1999, he clarified that one can only recognize irrational exuberance “after the fact.” Peter M. Graber accurately points out that “by denying its ability to predict, [Mr. Greenspan has] removed all meaningful content from the concept.” Basically, irrational exuberance means squat, and bubbles are only identified as such after the fact. We know nothing.

In 1926, Palgrave’s Dictionary of Political Economy defined bubbles as “any unsound undertaking accompanied by a high degree of speculation.” In line with the irrational exuberance definition, we only know if an undertaking is “unsound” and highly speculative once the bubble bursts.

All revolutionary, paradigm-shifting ideas, if pitched correctly, attract speculative capital. Some well-known bandwagons, such as internet stocks, electric vehicles, cannabis, and Bitcoin, promise revolutions in information, transportation, alternative medication, and economics, respectively. Speculative capital floods in, and only time can crystallize or dissolve these “revolutions.” Until time and the market declare a winner or loser, revolutions remain bubbles.

It is crucial to note that these revolutions transfer great wealth. The market handsomely rewards those who pioneered, crystallized revolutions.

As listed above, there are many crystallized revolutions that have accelerated humanity, and even more attempted revolutions. We must identify where those “revolutions” did not crystallize and truly were unsound undertakings with a high degree of speculation. Let’s examine the Tulip mania in the seventeenth century and overlay it with Bitcoin today.

Dutch Tulip Mania (1634-1637)

The epitome of bubbles is the Dutch Tulip Mania. When I first spoke with my dad about Bitcoin, he equated it to the value of a tulip.

Let’s touch on the important context of the seventeenth-century Netherlands.

The Eighty Years War, ending in 1648, between the Spanish and the Dutch was in full force. Six percent of the Dutch population was drafted, and war casualties, combined with the spread of the bubonic plague, caused a population decline of up to 50% in multiple regions.

Still, during much of this time, the Dutch conquered Brazil, built the majority of the world's merchant fleets, monopolized Japanese and East Indies trade routes, and founded New York.

Amsterdam was the financial center of the world. It was the New York City, London, and Hong Kong of the seventeenth century.

Just like today, regulators aim to keep markets stable and fair. In 1610, investment in futures markets for non-hedging purposes was heavily discouraged because of manipulative practices on equities. Though futures contracts weren’t necessarily banned, they were intentionally not legally enforceable in public courts.

But human nature prevails, and degenerates will gamble. Starting in 1634, novice retail traders began trading the novel tulip bulb. As the bubonic plague devastated Amsterdam, war raged, and people faced their mortality, long-term financial planning took a back seat.

There’s a range of bulbs that were traded, such as Zomerschoon, Gouda, Admirael Liefkens, Admiral van der Eyck, Semper Augustus, etc. The mania only applied to “beautiful broken bulbs'' and "single-color breeder bulbs.”

The demand for tulip bulbs began organically. French women would wear these tulips on the top of their dresses, and aristocrats would compete to give the most beautiful tulips to bachelorettes. For “piece” bulbs, the heavier the tulip (measured in aas, 1/20th of a gram), the more expensive. Wholesale tulip contracts were sold in units of ~1,000 azen (ass in plural). The contract value was dependent on the harvesting season ending in June and replanting in September. It was a revolution in fashion, beauty, and displays of wealth.

For the last year before its collapse in February 1637, tulip futures' markets were developed and became the tulip bulb's main investment vehicle. This mix of spot and futures price data mixed with different types, sizes, and qualities of bulbs makes the event difficult to accurately parse. Trades were often made unofficially in pubs called “colleges,” and premiums paid were called “wine money.”

At its peak, one tulip went for 1,000 guilders in a retail shop in Paris. While it’s incredibly difficult to factor guilders in the 1600s into current-day dollars, one calculation estimates it at $60k USD in 2016 dollars.

The chart below shows Gouda, a commonly traded bulb, and its price over the three-year bubble.

Since a lot of these contracts were unofficial and couldn’t be brought to public courts, profitable contracts at expiration became hard to enforce. There was also too much open interest for their books to accurately track amongst the colleges and notaries.

Recognizing the disorder and exuberance, a delegation of florists gathered on February 24th, 1637. They suggested executing all contracts pre-November 30th, 1636, and for later contracts, paying ten percent of the sale price to the seller. This was rejected.

On April 27th, 1637, the State of Holland called for the cancellation of all contracts, and the seller had the right to sell at market prices. The contract buyer had the option to terminate the contract at 3.5% of its value. Besides small local court cases and the occasional appraisal of a florist’s estate, no more data was available, and the party was over.

Bitcoin

While I won’t equate COVID to the bubonic plague or the Eighty Years War to global turmoil today, for the masses, the result is the same. Long-term financial planning is nearly nonexistent. Whether it be facing physical mortality or financial mortality, finances seem trivial in the scheme of life, and financial independence is near unattainable.

Most youth have little hope of a financial future and gamble on Bitcoin. While I believe in Bitcoin’s potential and blockchain as a technology, the “degen” (short for degenerate) market, for cryptocurrencies specifically, dwarfs the use-case market.

The average Bitcoin trader is more likely a lower-middle-class American than a third-world farmer who lives in a dollar-scarce economy. It does not mean Bitcoin’s potential cannot be realized, and the revolution will not crystallize. But, right now, this is realistically the landscape.

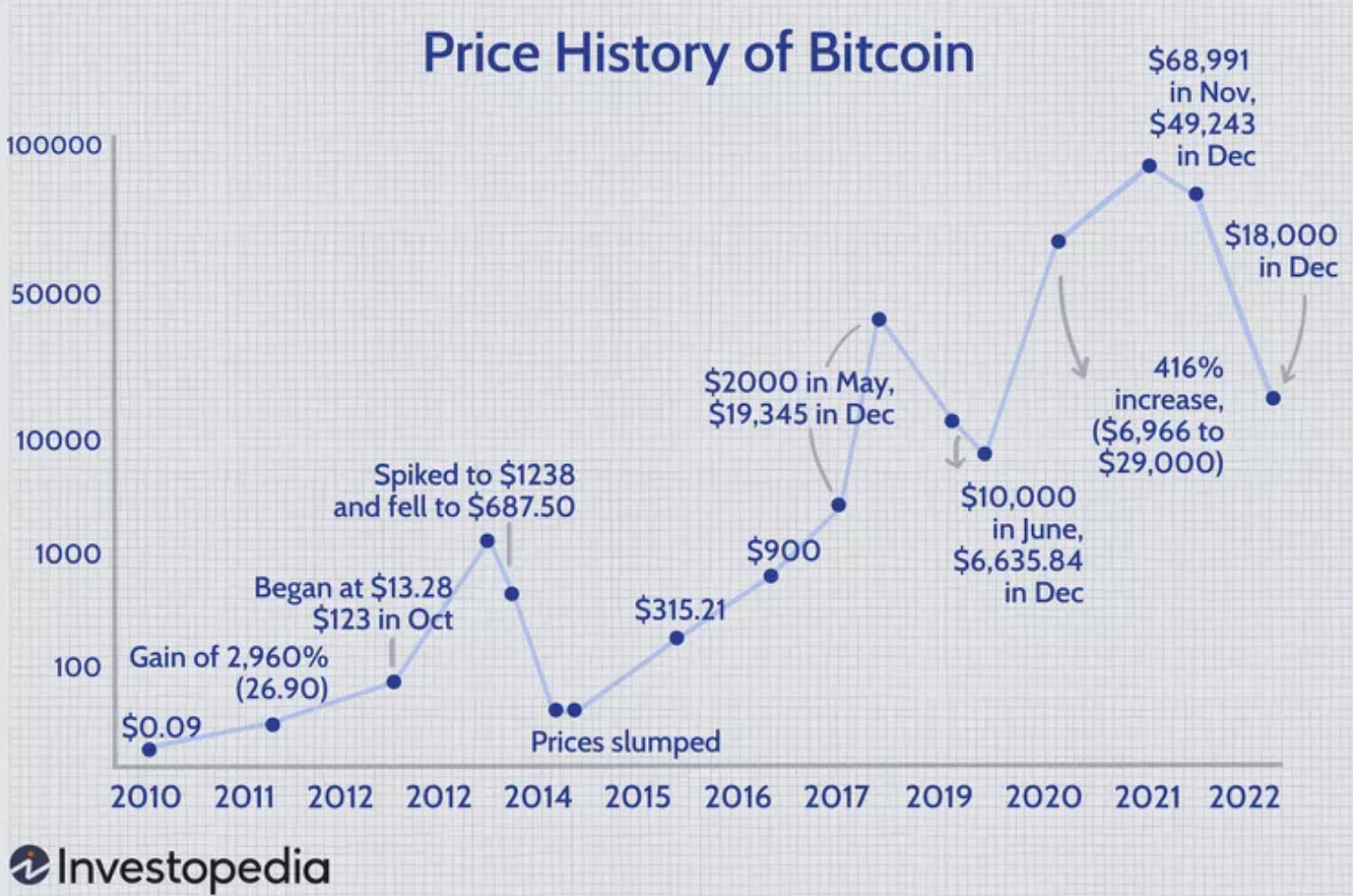

Since the first Bitcoin block mined in 2009, Bitcoin ($BTC) has remained immutable and exchanged with a sizable volume. Today, trading at $44k USD, Bitcoin's market cap peaked at $880 billion, with $1.5 trillion in all cryptocurrencies. This is comparable to an estimated $1.37 trillion market cap for silver. Regardless of how Bitcoin is viewed, it is undeniably resilient.

To ask the intrinsic value of Bitcoin or any other blockchain-based digital asset is a fair question. For the vast majority of human history, it was the correct question.

I could argue that the intrinsic value is the energy required to mine or compute it. It is the literal cost of energy, rig setup, expertise, etc. to mine it. The intrinsic value of a tulip bulb is the display of wealth and beauty.

But Bitcoin’s real value lies extrinsically. The extrinsic value is its utility in, let’s say, dollar-scarce countries or regions that lack stable alternatives. It is also censorship-resistant, outside-the-system money in a time when trust in governments is at an all-time low. While Bitcoin now trades in parity with US securities markets, it was not always like this and could decouple again.

As the free world gained food, economic, and moral stability, we valued land, commodities, and hard assets less. Tech companies have dominated and will continue to dominate the global economy. Google, Facebook, and Amazon are undeniably valuable. Why? Because of the utility they provide, not because of the hard assets they own. That utility leads to users, revenue, free cash flow, growth, and shareholder value. Their value lies in their utility, like Google with search, Facebook with social connectivity, and Amazon with merchant connectivity and cloud services.

Where’s the Bubble?

Let’s move a bit more theoretical, if we haven't already, and a bit more religious. Taught to me by Rabbi Ely Allen, Rabbi Avinoam Frankel writes in the Nefesh HaTzimTzum how it is amazing to see the Vilna Gaon’s (1720–1797) words “materialize” in our generation:

"There has been a dramatic shift in the world over the last 170 years or so, which has been very visibly accelerating within the most recent decades. This is perhaps seen in the most accentuated way by looking at the striking change in what the world attaches value to. For example, by looking at what types of assets the world's wealthiest people own, 170 years ago, they would have owned material assets such as land, property, and commodities. Currently, however, a significant number of them own intangible assets related to technology, software, medicine, the internet, and information. The world has become less physical and less material in its outlook, assigning constantly increasing value over time to the intangible over the tangible.”

Is it possible that the great Rabbinic minds from centuries ago have predicted Bitcoin’s rise and the trend towards intangible assets? Possibly.

Bitcoin is a revolution in how we have approached money, and only time will tell if it crystallizes. El Salvador has adopted BTC as legal tender, BTC ETF fillings are gaining steam, and unique BTC wallet holdings are at an all-time high. Bitcoin’s global impact is earning both main-street and wall-street adoption.

Unlike traditional tech movements but more like revolutions, Bitcoin has and needs to come user-up, not corporation-down.

Only history will tell if Bitcoin and cryptocurrencies as a whole are a bubble. One could argue that after over 14 years of Bitcoin gaining dominance and trillions of dollars invested in “web3”, the bubble is already over. It has been crystallized.

Equally, one can argue that with its intense volatility, Bitcoin has still yet to prove itself as an established and trusted store-of-value in the mainstream. I am hesitant to declare the battle won but to call it “irrational exuberance” or “a bubble” lacks substance.

Legislation ended the Tulip mania. Will legislation end Bitcoin? Is Bitcoin a bubble? Are tulips a fair comparison to Bitcoin? Time will crystallize all. But in the meantime, I will HODL.